The $10 Billion Insider Purchase

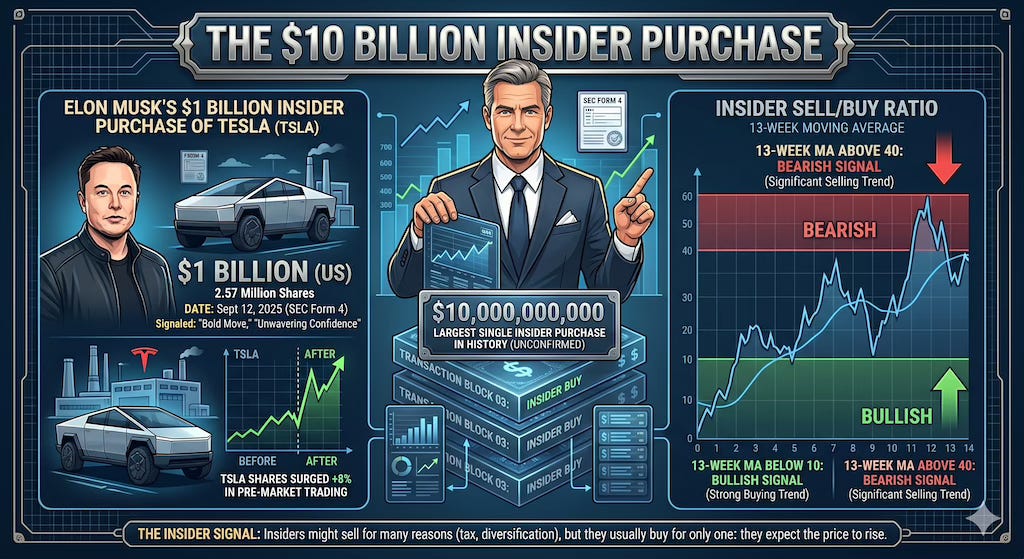

Last September we encountered the largest insider purchase we had ever seen in over 15 years of tracking insider buying and selling data. The $1 billion insider purchase reported through a Form 4 filing was so large that it significantly distorted the Insider Sell/Buy Ratio we calculate every weekend. The Insider Sell/Buy Ratio is calculated by dividing the total insider sales in a given week by the total insider purchases that week.

Insiders often sell way more stock than they purchase on the open market and on average insiders sell almost 30 times as much stock as they purchase each week. The week when we saw that $1 billion insider purchase, the Insider Sell/Buy Ratio dropped to just 3.47 and we covered Elon Musk’s purchase of Tesla (TSLA) in an Insider Weekends titled The Largest Insider Purchase Ever.

The only time we have seen aggregate insider buying exceed insider selling was during the COVID-19 pandemic and we wrote the following about that phenomenon:

We have been tracking insider data for nearly 10 years and in all this time we have not come across a single week where insider buying outpaced insider selling. The rapid drop in the markets over the last few weeks that saw the volatility index (VIX) jump to 75 last Thursday (the peak during the 2008-2009 Great Recession was 79) also caused insiders to start buying their own stocks at an accelerated pace.

We have been bearish for several weeks now and have written about showing restraint despite the insiders stepping up their insider buying because insiders as a group generally tend to be optimistic about their own companies, sometimes buy to “signal” the market and like value investors often tend to be early.

The following week when insider buying once again exceeded insider selling we wrote the following in an Insider Weekends article:

The market continued its decline last week but the volatility index or the “fear index” (VIX) also declined, indicating there was some exhaustion of the fear we were experiencing in the market. With the U.S. surpassing all other countries, besides China and Italy, in the number of confirmed COVID-19 cases, the news is likely to get worse over the next few days. On account of inadequate testing and lack of preparation, the number of cases in the U.S. is potentially significantly understated.

I have been unwinding the hedges I put in place more than a month ago, shorted the volatility index last week and plan to start nibbling on the long side from the COVID-19 watch list I wrote about earlier this month.

Imagine my surprise when I once again saw insider buying exceed insider selling earlier this month on account of a $10.52 billion purchase. This is more than 10 times the largest insider purchase we had ever seen until that point.

There are a lot of weird things that happen with Form 4 filings and sometimes they are just outright wrong. Some companies realize their mistakes and file an amended Form 4 later, and some don’t. This is one of the reasons we clean the data before we calculate the Insider Sell/Buy Ratio every Saturday. We then read the footnotes of Form 4 filings before we pick companies that land on our list of top five insider purchases and sales in our weekly Insider Weekends articles.

The first red flag when I saw this massive $10.52 billion purchase was that it was at a company with a market cap of less than $10 million. The second red flag was that this was a company that was located in Israel and was listed on the NASDAQ through American Depositary Shares (ADSs).

Foreign companies were previously exempt from reporting insider purchases and sales through Form 4 filings. For additional context you can check out Wharton Professor Daniel Taylor’s presentation to the SEC in this YouTube video about how foreign companies were not subject to a level playing field.

Starting in 2026 foreign companies that are registered on United States exchanges through American Depository Shares (ADSs) also have to report insider transactions through Form 4 filings.

Last month we started seeing several transactions by foreign companies we had not encountered before. One of the things we love about tracking insider transactions is that they help us discover new companies we might not have come across otherwise. There is a treasure hunt kind of excitement when I download all insider transactions for the week every Saturday morning and start working through the data.

While I was thrilled to find a bunch of international companies on my list, I also noticed there was several oddities in the Form 4 filings. In some cases these companies were reporting the purchase or sale price in local currency, while in others they were converting the prices to U.S. dollars.

Things got really difficult when they would report the number of shares in ordinary common shares instead of American Depositary Shares (ADSs) but the purchase price would be listed as the price of the ADS.

This was the case with that unusual $10.52 billion purchase filed for SaverOne 2014 Ltd (SVRE), a company that has seen its stock price drop by nearly 95% over the last year.

After multiple reverse splits, each ADS of the company now represents 43,200 ordinary common shares. Yikes!

Yes, each ADS in the U.S. that currently trades at a little over $4 represents tens of thousands of common shares. In the Form 4 filing, the number of shares purchased was reported as ordinary shares but the price reported was that of the ADS. This made it appear that the insider had purchased over $10 billion worth of stock.

To the company’s credit, they did mention this weird mismatch and also thankfully provided the common shares to ADS ratio of 43,200:1 in the footnotes of the Form 4 filing. Once I recalculated the purchase, it shrank to a more reasonable $243,541.

If this weren’t enough, there are instances where a single filing will include purchases in both common share prices and ADS prices. For example, each ADS of the Australian biotech company Mesoblast Limited (MESO) represents 10 ordinary common shares listed in Australia. The ADS price is therefore typically about ten times the underlying share price.

One Form 4 filing related to a purchase by 10% owner and Director Gregory George mingled both common share prices and ADS prices in the same filing.

In other words, the complexity of working with Form 4 data has jumped up several notches. Any headlines you see about big spikes in either insider purchases or sales should be scrutinized closely.

For my fellow Form 4 warriors, your job has gotten harder but there is treasure in them thar hills.

Disclaimer: Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.