End of the Road

“Our greatest glory is not in never failing, but in rising every time we fail.” – Confucius

“It’s fine to celebrate success, but it is more important to heed the lessons of failure” – Bill Gates

A few days ago, the Wall Street Journal reported that Spirit Airlines (SAVE) was potentially exploring bankruptcy as the discount airline struggles with a debt load of $3.3 billion. While many factors are likely at play, the top one that comes to mind for most investors is regulators blocking the acquisition of Spirit Airlines by JetBlue (JBLU). You can check out all the gory details of that failed merger in our deal postmortem here.

This situation reminded me of the pharmacy chain Rite Aid, which declared bankruptcy in October 2023. This was another case of a struggling company that would have benefited from merging with a larger company like Walgreens (WBA) but was instead put through the regulatory wringer in 2016 and 2017. More than 20 months after that deal was announced, the companies eventually called off their merger.

Antitrust has an important role to play to ensure consumers are not harmed through the creation of monopolies or duopolies with complete pricing power. This happened in India when Pepsi (PEP) and Coca-Cola (KO) re-entered the market in 1989 and 1993. The most popular local soft drink brands like Thumbs Up, Limca and Gold Spot were all acquired by Coke and other brands like Campa fell by the wayside. You can check out the fascinating history of the Indian cola wars here.

Just like prosecutorial overreach, regulators can become overzealous in blocking deals. Sometimes it is because they are attempting to protect consumers (Spirit Airlines, Rite Aid, Albertsons), sometimes it is to protect jobs (U.S. Steel) and at other times it is for national security reasons (Lattice Semiconductor).

This June, one of the five FTC commissioners wrote the following strongly worded dissenting statement in opposition to the FTC’s plan to ban noncompete clauses:

On April 23, 2024, the Commission promulgated the Non-Compete Clause Rule (“Final Rule”).1 It bans all employee noncompete agreements—agreements in which an employee agrees not to work for his or her employer’s competitor after his or her employment. It is by far the most extraordinary assertion of authority in the Commission’s history. It categorically prohibits a business practice that has been lawful for centuries. It invalidates thirty million existing contracts. It redistributes nearly half a trillion dollars of wealth. And it preempts the law of forty- six States. It does all of this on the basis of a few words in a 110-year-old statute—the Federal Trade Commission Act (“FTC Act”)2—words that the Commission had never used to regulate noncompete agreements until the day before this rulemaking began.

Whatever the Final Rule’s wisdom as a matter of public policy, it is unlawful. Congress has not authorized us to issue it. The Constitution forbids it. And it violates the basic requirements of the Administrative Procedure Act.

I therefore respectfully dissent.

One commissioner, Christine Wilson, went so far as to resign from her role in a noisy exit that included penning a WSJ opinion piece. If the FTC wants to go beyond harm to consumers and make the case for loss of jobs as a result of consolidation, they should also take into account the impact of job losses when struggling companies like Rite Aid, Spirit Airlines and iRobot (IRBT) are blocked from merging with stronger companies. These companies have to resort to large layoffs and bankruptcy.

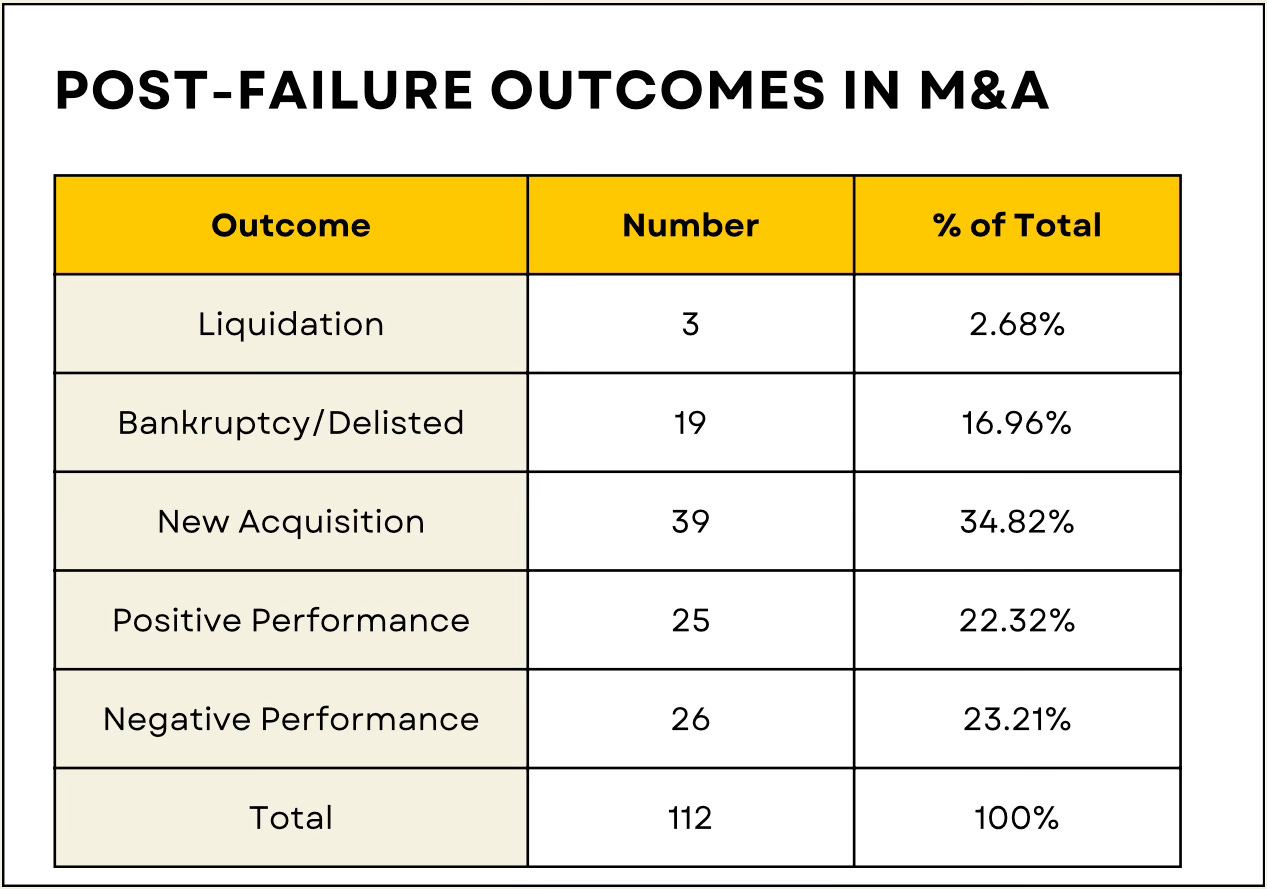

Following the potential bankruptcy speculation related to Spirit Airlines, I was curious to see how companies that had experienced a collapsed deal, performed post-failure. We provide our premium subscribers with access to a list of over 110 failed mergers spanning nearly 15 years of data.

I downloaded this list and examined the data to see if the general consensus among investors about selling a company if a merger does not work out holds true. I’ve classified the results in the following table.

Source: InsideArbitrage

The results surprised me on multiple levels. More than 57% of these failed deals had positive outcomes where the post-failure performance was positive or resulted in a new acquisition. The average gains of the positive performers was 155.17% and a median gain on 90.19%. As is often the case, there were some strong performers like KLA-Tencor Corporation (KLAC) with a gain of over 1,000% and Lattice Semiconductor Corporation (LSCC) with a gain of almost 808% post-deal failure that skewed the results.

The liquidation situations probably yielded some minor payout to shareholders but all the bankruptcy situations resulted in a near 100% loss. The negative performers had an average loss of 43.92% and a median loss of 49.76%.

My analysis is not complete because it would be important to figure out the gains or losses of the nearly 35% of deals that received a new offer and completed a successful merger. More importantly, since these 112 deals failed during various times over the last 15 years, the gains or losses need to be annualized and compared to an appropriate index to get a full picture of how someone would have performed by holding on to this basket of stocks.

Looking at these results on the surface, it looks like the general consensus of selling after a deal failure appears to be correct. However considering more than half of them had positive outcomes, failed deals could provide good hunting grounds, especially in the period immediately after deal failure when forced selling temporarily depresses prices. I hope to dive deeper into the data in the future to see if I can derive additional insights.

Great post. For those listed as positive/negative performance what time frame are you looking at post deal failure?