Concentrated Merger Arbitrage Funds – Q4 2024 Update

This is our sixth update about new merger arbitrage related positions at funds that tend to have concentrated positions in their portfolio. You can find our first update here and our Q3 2024 update here. I mentioned the following in our last update about the number and kind of funds I am tracking:

“This has been a challenging year for merger arbitrage with multiple widely followed deals like Capri (CPRI) failing. Beyond the hit to my personal portfolio, I also saw the impact on the professional investors I follow who focus on risk arbitrage. When I first started this series of articles, I was tracking eight funds but one of them closed shop and I am dropping one more this quarter because their portfolio is more diversified and not concentrated in their top 10 positions. A third fund saw their concentration in the top 10 positions drop to 46% but I am going to retain them for now.

I am also starting to see increased reliance on options to either hedge positions or juice returns as well as some style drift. One of them started a new position in Vestis (VSTS), the company that was spun out of Aramark, although to be fair there was a rumor in September that Vestis might get acquired.”

There are currently 79 active M&A situations in the U.S. ranging from highly risky deals like the $14.9 billion acquisition of United States Steel (X) by Nippon Steel that is trading at a spread (potential profit) of nearly 44% to the acquisition of Endeavor Group (EDR) by Silver Lake in a $13 billion deal, which is trading at a negative spread of over 10%

Deal With a Negative Spread

It’s quite rare that you see merger arbitrage deals with a negative spread, especially when there are no special dividends or CVRs attached to the price, as is the case with the Silver Lake and Endeavor deal. Negative spreads often occur when shareholders are dissatisfied with the deal price and are hoping to get a higher offer. Endeavor is currently trading at around $30 per share, which represents a negative 10% spread on the deal.

Endeavor and Silver Lake are able to bypass the minority shareholder vote since common stock shareholders of Endeavor don’t have significant voting rights. When Endeavor went through with its 2021 IPO, the company split itself into a complex structure of five classes of shares. Ultimately, common stock shareholders, meaning the shares that you or I could buy on the open market (Class A shares), gives us only about 0.4% to 0.5% of voting rights. Class Y shares, on the other hand, have immense voting powers. And together, Silver Lake, Endeavor’s CEO, Ariel Emanuel, and Executive Chairman Patrick Whitesell own 91.5 % of Endeavor’s voting stock.

Endeavor owns a significant stake in TKO Group Holdings (59% after certain transactions between them close) and with the rise in TKO’s (TKO) stock over the last few weeks, the Silver Lake acquisition feels like highway robbery.

Types of Funds Tracked

The concentrated funds I like to track prefer to pick and choose among those situations and tend to concentrate more than 50% of their portfolio in their top 10 positions. To reiterate what we wrote about 13F filings in our first article:

“Investment firms with over $100 million in assets are required to file form 13F with the SEC within 45 days after the end of each quarter. This filing provides a small window into the fund manager’s portfolio and is a great source for new investment ideas. You also end up with information that is potentially stale and as many investors have come to find out, you can’t just follow someone else into an idea without doing your own deep due diligence. The Gurus section of InsideArbitrage includes curated lists of professional investors and fund managers categorized based on their investment style.

We are currently tracking 49 event-driven funds of various sizes. There are firms with just 3 positions in their 13F portfolio and others with thousands of positions. This does not mean the former has their entire portfolio is just 3 positions as they may have exposure to other positions, including private companies, which don’t have to be reported on the 13F form.”

New Additions

I am going to focus on some of the new additions across the six funds I am tracking. The funds are continuing to use options to either protect downside or juice returns on the upside but I saw less pre-deal activity. I am excluding deals like the acquisition of Summit Materials (SUM) by Quikrete that several of these funds had a position in but that closed after the end of Q4 2024.

The $6.7 billion acquisition of Arcadium Lithium (ALTM) by Rio Tinto Group (RIO) for $5.85 per share in cash was a new position for five out of the six funds. The spread at one point after announcement was 20.62%. It is currently under 0.50% as all regulatory approvals have been received and the companies expect the deal to close by March 6, 2025. Rumors of this deal came out on Friday, October 4, 2024 and the deal was confirmed on Wednesday, October 9, 2024.

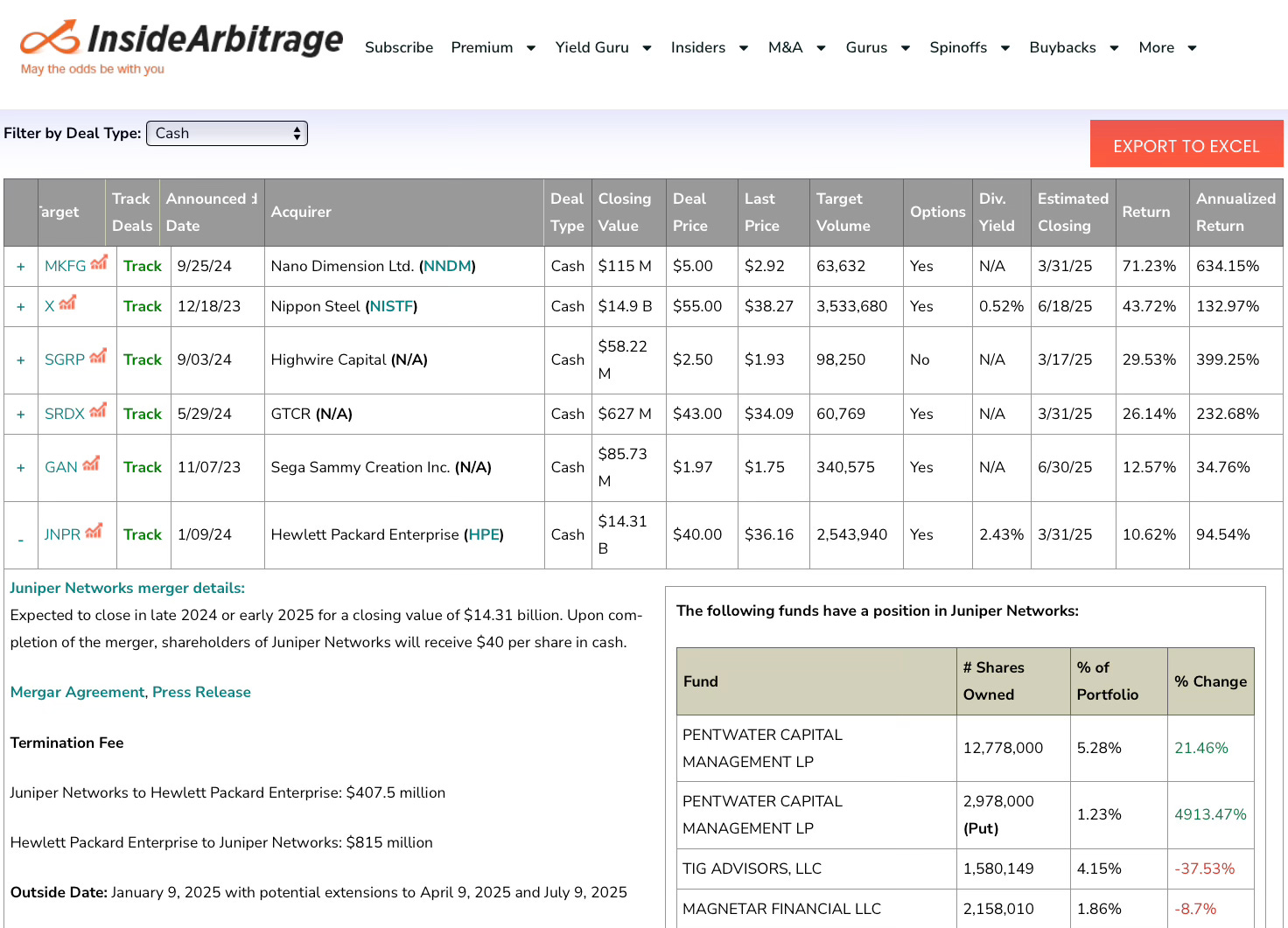

When reviewing new Q1 2024 positions for these six funds, all of them had a position in the $14.31 billion acquisition of Juniper Networks (JNPR) by Hewlett Packard Enterprise (HPE) for $40 per share in cash. Four of these funds added put options on Juniper Networks in Q4 2024. The spread on the deal had spiked in mid-November on concerns the DOJ might challenge the deal. The DOJ finally sued to block the deal on January 30, 2025.

The $16.8 billion acquisition of Aspen Technology, Inc. (AZPN) by Emerson Electric (EMR) for $265.00 per share in cash was a new position for three funds. The stock is trading very close to the acquisition price but it could be a free call option if Elliott Management, who owns almost 10% of Aspen Technology, is successful in getting a higher price for Aspen shareholders.

Capital One Financial’s (COF) massive $35.3 billion all stock deal for Discovery Financial Services (DFS) was a new position for two funds. I usually skip situations where only two funds started a new position but in this case, four funds had a position in DFS in Q1 2024. Two of them then exited the position and they are back in again in Q4 2024.

It is also worth mentioning that one fund joined three others in starting positions in both Spirit Aerosystems (SPR) with a spread of 8.49% and Frontier Communications (FYBR) with a spread of 7.71%. The fund that started a position in Frontier Communications also added put options.

If you want to stay on top of both pre-deal situations and announced deals, we offer alerts by email for new deals and rumored deals, a daily event-driven monitor that covers all activity across multiple event-driven situations and multiple tools like our merger arbitrage tool and the deals-in-the-works tool. Check out the various plans we offer here or reach out to me for a free two week trial.

Disclaimer: Among active merger arbitrage related situations, I currently hold a long position in First Financial Northwest (FFNW). Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.