C-Suite Transitions: A Deep Dive into CEO Changes

Earlier this week, our intern Luke Hammerschmidt shared the results of his deep dive into C-Suite transitions and especially CEO and CFO changes in a live webinar. In case you missed the webinar, you can check out the recording here (passcode: H064t.@G) and download a PDF of the slides he presented here.

Methodology

Luke started his project related to the impact of management transitions by segmenting our data based on the size of the company, the industry it operates in and more. He then reviewed the outcomes of CEO transitions across various time periods (from three months through three years) for those segments using our C-Suite Performance Report.

He did this for several weeks to build intuition and we reviewed the results together to see if we could find any patterns. He then pivoted to using Google’s NotebookLM tool to ingest as many as 40 academic papers and other resources related to management transitions and generated a meta-analysis that surfaced some really interesting insights.

The three insights that in some cases reinforced intuition I had about C-Suite transitions and in others surprised me, were:

Boomerang CEOs, the ones that had a storied past with the company and were brought back again to turn it around, in aggregate did not perform very well. There were exceptions like Steve Jobs’ return to Apple (AAPL) or Howard Schultz taking over the reins at Starbucks (SBUX), but they are not representative of how most boomerang CEOs perform.

New CEOs in turnaround situations often front-load all the bad news in a “big bath” quarter and the subsequent outperformance of the company after this event is significant over a 12-month period.

Sudden CFO resignations without a named successor could be the canary in the coal mine, signaling that revelations of fraud, an admission of weak internal controls or an accounting restatement are around the corner.

The aftermath of the dot-com bubble of the late 1990s didn’t just lead to a massive decline in the NASDAQ and associated tech companies, but it also led to the unraveling of the golden age of fraud. It wasn’t just investors that were hurt when fraud was uncovered in companies like Enron and WorldCom in 2001 and 2002, but many employees at these companies who had their retirement savings invested almost entirely in their company’s stock were also wiped out.

The collapse of these large companies and Enron’s auditor Arthur Andersen triggered the passing of the Sarbanes-Oxley Act (SOX) in 2002 to restore public trust in corporate financial reporting. One of the provisions of this act was that senior company executives like CEOs and CFOs had to personally certify the company’s financial statements.

Executives who certified false financial reports faced not only large fines, but also anywhere from 10 years to 20 years in prison depending on whether the certification was done knowingly or willfully. This massive liability ties back to the third insight mentioned above related to sudden CFO resignations. CFOs would much rather resign and walk away from a highly compensated position than deal with the risk of jail time if they are not comfortable certifying the company’s financial statements.

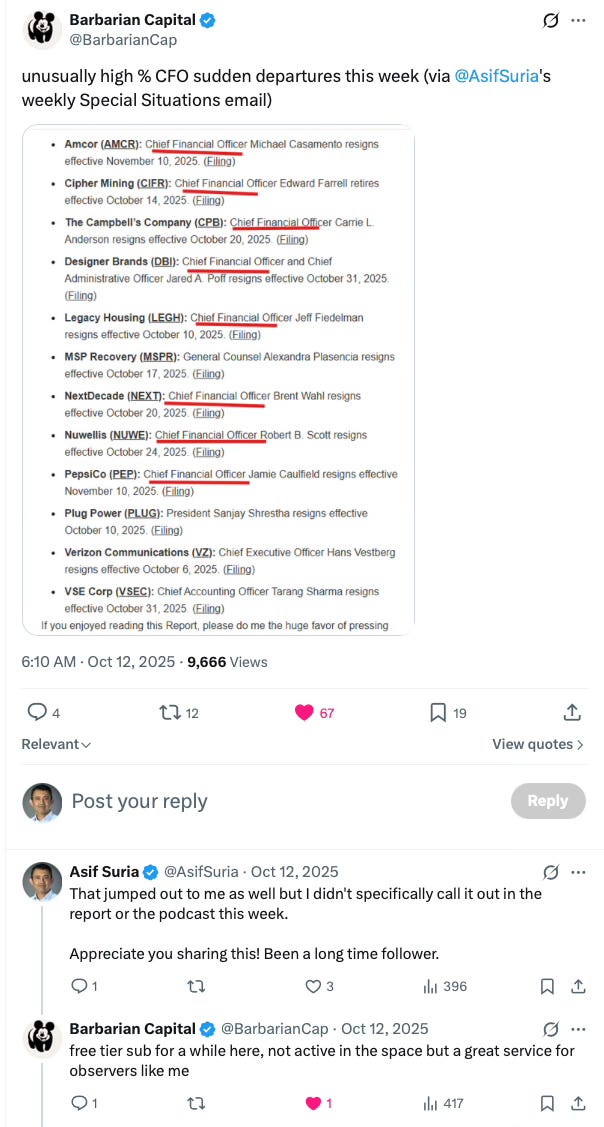

If you think sudden CFO resignations are rare, you would be surprised to learn that there were three just last week. In some weeks, we have seen nearly 10 sudden CFO departures as you can see from this tweet.

Whether it is a new CEO at the helm of one of your portfolio companies or the sudden departure of the CFO, the work Luke has done and shared in his webinar will give you a framework to think about how these changes are likely to impact your portfolio.

If you like his webinar or the slides, you can connect with him on LinkedIn or drop him an email.

Disclaimer: Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.