Armanino Foods of Distinction and Crexendo From The Planet MicroCap Conference

I was at the Planet MicroCap conference in Las Vegas last week where I participated in a special situations-focused panel discussion with Rich Howe and Colin King. I am thankful to both Robert Kraft and Ian Cassel for inviting me to this conference and giving the three of us a chance to share ideas and ask questions about how each of us approach special situations. In many ways, we did on stage what we normally do privately or on our podcasts.

The conference was a lot of fun and I got a chance to catch presentations by Kingsway Corporation (KWY), Pro-Dex (PDEX) and several other companies. What is even more fun is reconnecting with old friends like Sam Namiri, who was recently a guest on Robert’s Planet MicroCap podcast as well as making new friends like Sandeep Singh, Andrei, Alex Cho-Kee and Matt.

I also got a chance to meet with the management teams of a few companies and I wanted to highlight two of them, Armanino Foods (OTC: ARMN) and Crexendo (CXDO).

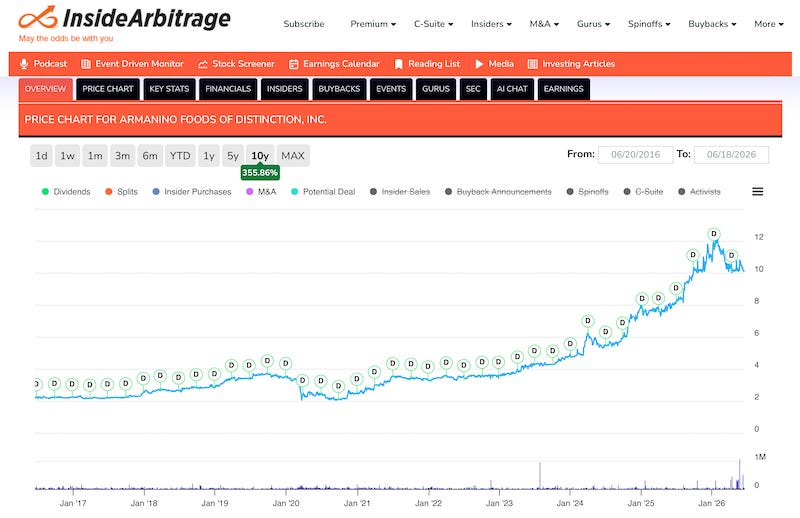

Armanino Foods of Distinction (OTC: ARMF): $10.20

Market Cap: $317M

For several years, my friend Adib Motiwala has been telling me about one of the largest pesto sauce producers in the U.S., Armanino Foods. The position has been a multi-bagger for his portfolio and while the story sounded interesting, it didn’t fit my event-driven framework. Moreover the stock is traded over-the-counter and I usually don’t invest in OTC stocks.

He mentioned that the company’s production facilities were across the bridge from where I lived in the San Francisco Bay Area and that I should check them out. When I noticed that they were going to be at the Planet Microcap conference, I figured it would be a good idea to learn more about the company. The company, which was family run, hired a new professional CEO last year who previously worked for PepsiCo (PEP). She onboarded a new CFO with an investment banking background six months ago.

C-suite transitions are events we pay attention to and given the background of the new CFO, the potential of an uplisting to an exchange like NASDAQ or NYSE could be another catalyst that would make the situation interesting for me. Considering their production facilities in Hayward, California are just a 15 to 20 minute drive away from where I live, I plan to drive over and check them out. I mentioned to the CEO that I might bring my daughter along as she is a huge fan of pesto sauce.

Armanino Foods produces 250 kinds of sauces that you are likely to find in the frozen foods aisle at grocery stores like Safeway and Albertsons. I was surprised to learn that I would find their sauce in the frozen foods section, and both the CEO Deanna and another professional investor who was in the meeting, explained that the best pesto sauces are usually not found on regular shelves.

This is not a deep dive on Armanino Foods like we do for our spotlight ideas in our monthly special situations newsletters but a quick look at the company. There are five things about the company that stood out to me:

They are the largest basil pesto sauce producer in the U.S. with 60% market share. The next largest producer has 6% market share.

90% of their business comes from food service and 10% from retail locations like Safeway, Lucky’s and Costco Business Center.

Gross margin of nearly 50% and operating margin of over 30% is unusually high for a packaged food company.

They recently leased a new 90,000 square foot facility in Mountain House, California because their existing 26,000 square foot facility in Hayward, California is nearly at capacity.

They have a presence in Japan but plan to expand to multiple countries. This will bring down margins over time.

I said five things but it is hard not to mention this sixth point. Given the new CEO’s sixteen years of experience at Pepsi, she plans to target quick service restaurants (QSRs as the industry likes to call them) like McDonald’s, Chipotle and others to drive revenue growth.

Crexendo (CXDO): $6.92

Market Cap: $224M

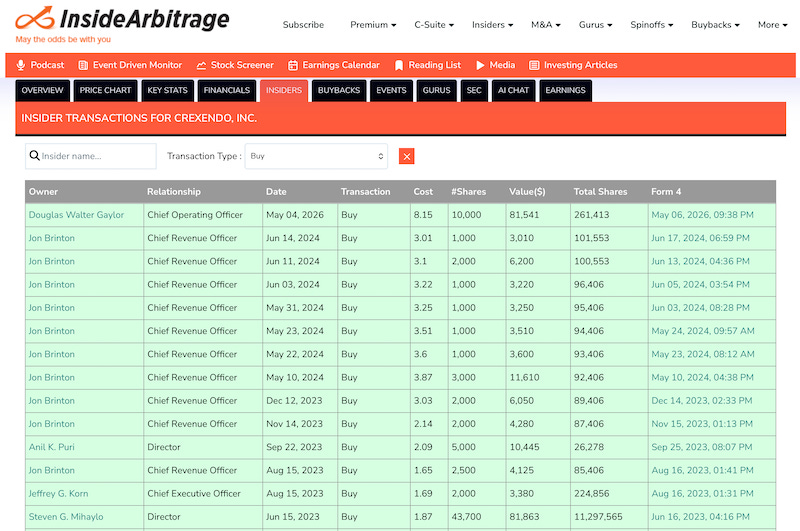

Before meeting with the management team of Crexendo at the Planet Microcap conference, I happened to look at open market purchases by the company’s insiders. As you can see from this link and the image below, several insiders purchased a small number of shares in very well-timed transactions in 2023 and 2024. However one insider, COO Doug Gaylor, also purchased shares last month, after the stock had appreciated quite significantly.

I opened the Form 4 filing and a closer look revealed that the purchase was most likely a sale that was mistakenly filed as a purchase. As it turns out, the folks who were meeting with me were COO Doug Gaylor and CFO Ron Vincent. I showed them the filing and they agreed that it was a mistake that would be fixed through an amended filing.

Crexendo is a company that provides telecommunication services to clients much the same way that companies like RingCentral (RNG), Vonage (acquired by Ericsson for $6.2 billion), 8×8 (EGHT) and Ooma (OOMA). If that was all the company did, I would not have written about them but it was the other part of their business that really caught my attention.

Beyond providing services to retail clients, they also provide a software platform (the wholesale business) that companies can use to provide their own telecommunication services. They have 245 licensees of this platform and their only competition in this space comes from Cisco BroadSoft (about 1,000 licensees) and Microsoft, which sold its Metaswitch division to Alianza (800 licensees).

BroadSoft is no longer a core focus of Cisco and this has provided an opportunity for Crexendo to poach some of these customers from Cisco. Microsoft was planning on sunsetting their Metaswitch division but decided to instead sell it to Alianza.

Just like I did with Armanino Foods, instead of doing a deep dive into Crexendo, I am going to highlight five things about the company that stood out to me:

Crexendo picked up 14 licensees for its software platform last year and nine of them came from either BroadSoft or Metaswitch. They haven’t lost a single customer to either of those platforms in seven years.

The management team appears to have long tenures and COO Doug Gaylor has been with the company since 2009, while CFO Ron Vincent has been with the company since 2012.

The company saw 28% organic growth on the wholesale side last year and 12% in Q1 2026. Organic growth on the retail side was 15% in Q1 2026 but that was helped by a $1 million one-time jump. Historically the retail side has grown 7% year-over-year.

AI is a tailwind for the company as they already have a per session revenue model compared to competitors that still have a per seat model. They released their AI receptionist called Crexendo AI Receptionist Operator (CAIRO) in January and expect their average revenue per retail customer to increase by 40% due to contribution from CAIRO (very cool acronym).

I tried to highlight to Crexendo that they could take this one step further and reposition themselves as a communication layer for AI agents much the same way Salesforce’s Slack or Twilio’s messaging APIs have become preferred choices for agentic communications.

It was too hard to stop at five points and I wanted to highlight their recent ESI acquisition. ESI is a company with $26 million in revenue that had been licensing Crexendo’s software platform for 14 years. Crexendo purchased ESI for a very attractive 1.25 times forward revenue with $27M paid through cash on hand and $8M in stock. Other licensees like ESI represent a fertile fishing pond for future acquisitions.

I don’t have a position in Armanino Foods or Crexendo but will most likely start a position in Crexendo in the coming weeks after I complete my due diligence on the company. I figured I would shares some early thoughts in case other investors are also following these companies and would like to compare notes.

Disclaimer: Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.