This article is about a merger arbitrage focused fund that recently made what I consider one of the greatest trades ever and it turns out that the trade was not even a merger arbitrage situation. Before we discuss that fund and its trade, we are going to pay homage to the OG of merger arbitrage, John Paulson, who was once called “the king of merger arbitrage”.

We will discuss three investments by Paulson and then get to a trade that could be a worthy successor to the one discussed in the book The Greatest Trade Ever.

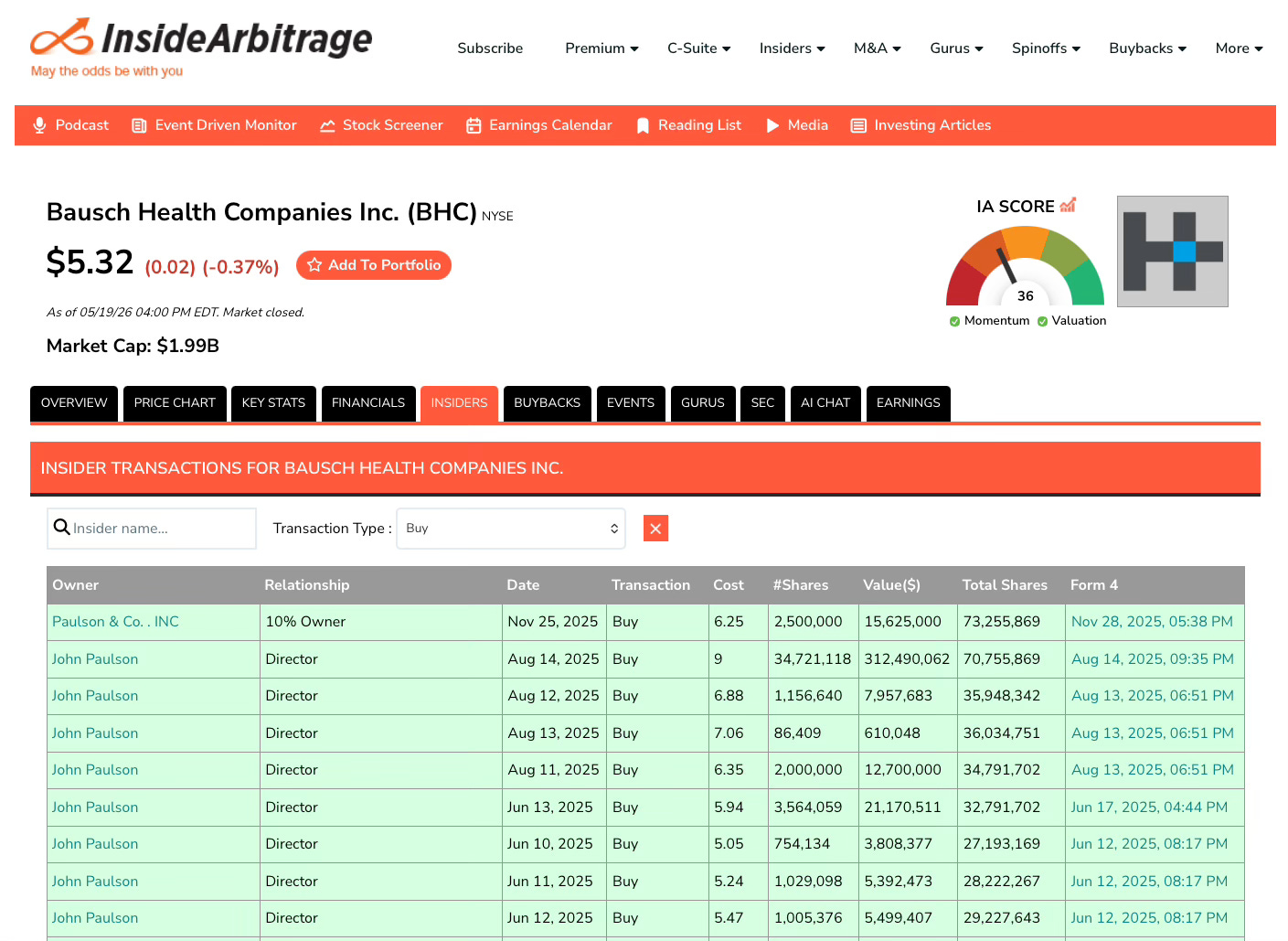

In an Insider Weekends article Tamanna wrote a little less than a year ago, we discussed an insider purchase of Bausch Health Companies (BHC), a company that was previously know as Valeant Pharmaceuticals and was sometimes referred to as the “Enron of pharma”. While Bausch Health didn’t interest us much, what really stood out to us was the person buying the stock and we wrote the following about John Paulson:

“The market paying attention to John Paulson isn’t all that surprising. One of the first books I read about investing was The Man Who Solved the Market by Gregory Zuckerman. Mr. Zuckerman also wrote a book called The Greatest Trade Ever – which tells the story of how the hedge fund manager John Paulson (who had a background in special situations and M&A) bet against risky mortgages in 2006 and onwards, accurately timing the implosion of the housing market and the Great Recession, making more than $15 billion for his firm.

Mr. Paulson then went on to invest very heavily in gold, something he remains invested in today – looking at the snapshot of his portfolio as provided by his 13F filing. Other interesting things to note is that over 40% of his portfolio is invested in a single company, Madrigal Pharmaceuticals (MDGL) and that Bausch makes up approximately 7% of the portfolio. Naturally, a purchase from an insider with such a successful track record who has been with the Board since 2017 is a good signal, but we’re not fully seeing the thesis when it comes to a company with such a massive debt balance and slowing revenue growth.

It is also important to remember that after “The Greatest Trade Ever”, Paulson’s bet on rising inflation and his investments in gold didn’t play out the way he expected, leading to years of subpar performance. After a 26 year run, he returned external capital to investors in 2020 and converted the firm into a family office.”

A week after his Bausch Health purchase, he made an appearance in another Insider Weekends article when he added to his stake in Perpetua Resources (PPTA) and some of what we discussed about that purchase is as follows:

“We typically don’t include purchases from 10% owners as part of our list of top five insider buys and sells because although the SEC considers them to be insiders (and thus requires that 10% owners file Form 4s), they aren’t really involved with the inner workings and operations of a company in the same way in which the C-Suite team or some directors may be. Nevertheless, we made an exception for John Paulson on account of his past insider activity.

Perpetua Resources makes up over 15% of Mr. Paulson’s portfolio, and given that he’s filing a Form 4 as a 10% owner, he obviously has a major stake in the business. His nearly $100 million addition to his Perpetua position this week is surprising for a number of reasons. Firstly, Perpetua has a market cap of just $1.35 billion – Mr. Paulson is effectively purchasing 7.4% of the company through this transaction, a massive purchase by any measure.

Furthermore, Perpetua’s stock has risen by over 100% in the last year alone and the stock price very recently hit an all-time high. The fact that Mr. Paulson is picking up shares at a time where the stock price has already appreciated so much is peculiar.

Part of the extreme rally can be explained by macroeconomic conditions. Perpetua is a exploration-phase mining company, primarily involved with mining gold and silver, but the company also engages in the exploration for and mining of the metal antimony. Antimony is a naturally occurring, silvery-white metalloid, primarily used in alloys to enhance their strength and hardness, particularly in lead-acid batteries. It’s also a key component in flame retardants and is used in the semiconductor industry. Thus, antimony has applications ranging from technology and defense applications to grid capacity storage batteries. However, the US has no domestically mined source of antimony and China, Russia and Tajikistan control more than 90% of global production.

China has started to restrict exports of antimony to the United States, which makes finding a domestic source of antimony all the more important. Perpetua, via their Stibnite Gold Project, has one of the largest economic reserves of antimony and could supply approximately 35% of U.S. demand in the first six years of production. More can be read about the project at this link, and a more complete overview of Perpetua can be seen in the image below.”

About two months later, John Paulson made an appearance in one of our Insider Weekends articles for the fourth time (the third time was a block purchase of Bausch Health from Carl Icahn). This time it was because one of the most successful biotech hedge funds was buying Madrigal Pharmaceuticals (MDGL), a company in which John Paulson had a significant stake. Given below is a small part of what we wrote about Madrigal:

Madrigal Pharmaceuticals’ Key Investors

Before we get into Madrigal Pharmaceuticals and the kinds of drugs it develops, we wanted to take a moment to dive into Baker Brothers. The hedge fund was founded in 2000 by brothers Julian and Felix Baker, and is known for its extreme secrecy (the Baker Brothers notably avoid the press at all costs, and the fund itself has no website or real online presence).

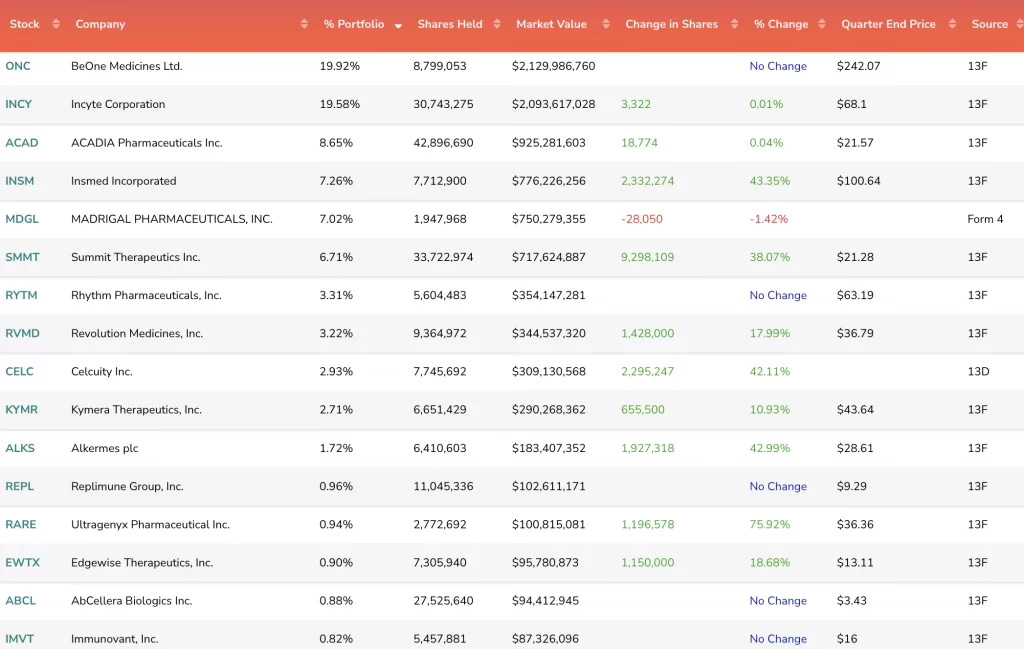

In 1994, the pair started managing healthcare investments for the Tisch family, the namesake for the NYU Tisch School and the family best known for turning the theater chain Loews (L) into a massive conglomerate. The Bakers created a standalone business in 2000 and within six years, they oversaw about $1 billion as an exclusively biotech-focused investment firm. As it stands today, Baker Brothers Advisors has AUM of $21.98 billion, and a snapshot of their top holdings as given by their most recent 13F filing can be seen in the image below.

The firm counts Yale University’s endowment as one of their biggest investors, and the university must be pleased with the way many of the Baker Brothers investments have turned out – the two made $1.4 billion in two weeks in 2019 after massive successes at Seattle Genetics (later renamed Seagen and acquired by Pzifer (PFE) for $43 billion in 2023) and BeiGene (ONC).

We frequently see insider purchases from the Baker Brothers at various companies in their portfolio, but Madrigal is one of their largest positions. Given Paulson’s involvement in the business, the fact that the company’s stock has run up by over 62% in the last year alone, and that Julian Baker serves as the Chairman of the company’s Board, we figured a closer look at Madrigal Pharmaceuticals was warranted.

Madrigal Pharmaceuticals

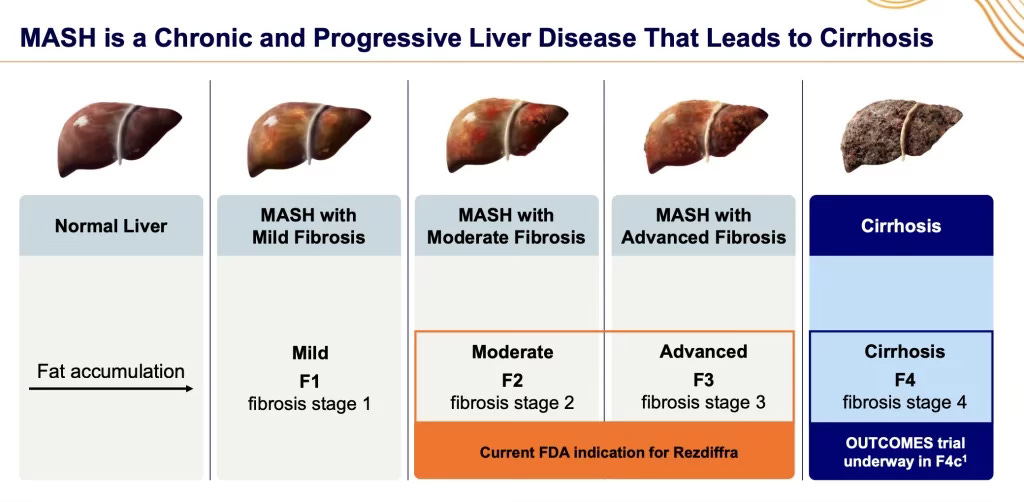

Madrigal is a biopharmaceutical company focused on treating metabolic dysfunction-associated steatohepatitis (MASH), a progressive liver disease that can lead to cirrhosis, liver failure, and death. A full explanation of the disease and its different stages can be seen in the image below. Founded in 2006, the company achieved a major milestone in 2024 by becoming the first company to receive U.S. FDA approval to treat MASH via its therapy Rezdiffra. Until mid-August 2025, Madrigal enjoyed exclusivity in this market – but on August 15th, the FDA approved Novo Nordisk’s (NVO) GLP-1 drug Wegovy to treat MASH in adults with moderate-to-advanced fibrosis. Wegovy was intially approved in 2017 for the treatment of obesity to reduce the risk of cardiovascular events, but this additional approval expands the scope of the drug much further.

However, there are many differences between the two drugs that maintain Madrigal’s more dominant position in the market. Rezdiffra is an oral tablet as opposed to Wegovy’s injection, which is a lot easier on patients, and has a liver-specific drug mechanism, whereas Wegovy is primarily meant to regulate glucose and appetite, with liver benefits as a secondary effect of overall weight loss. Wegovy intends to improve MASH through anti-inflammatory effects and by reducing fat levels in the liver.

How did John Paulson’s Investments Turn Out?

Paulson started his buying of Bausch Health at prices that ranged from $5.05 to as high as $9.00 and he paid a premium to buy a stake from Carl Icahn in a privately negotiated transaction at $9.00 per share. In that context, with Bausch Health currently trading at $5.32, he is down more than 35% on those 2025 purchases.

The story looks much better when you look at how he did with Perpetua Resources, which is up nearly 87% since his June 2025 purchase. He is likely also pleased that Madrigal Pharmaceuticals is up 76% over the last year and it is currently his second largest position, as can be seen from his holdings based on a 13F filing that came out last Friday. It looks like he used this jump in the stock to scale back some exposure to the company. Funds have to file a 13F with the SEC within 45 days after the end of a quarter (May 15 for Q1 2026) if they have $100 million of 13F securities (stocks, ETFs, certain options, etc.).

Over the last two years the 13F portfolio value for Paulson & Co, which does not include international stocks, short positions and other types of investments that don’t have to be reported on 13F filings, has more than doubled from $1.45 billion in Q1 2024 to $3.11 billion in Q1 2026.

Which brings us to another merger arbitrage focused fund that has seen its 13F portfolio value also nearly double from $9.76 billion in Q1 2024 to $19.28 billion in Q1 2026.

The Avis Budget Group Trade by Pentwater Capital

The car rental company Avis Budget Group (CAR) was a case study in my Stock Buybacks chapter of my book The Event-Driven Edge in Investingand I mentioned the following about their share repurchases:

“Over a two-year period in 2021 and 2022, Avis Budget Group retired nearly a third of its shares outstanding through buybacks. The company’s diluted shares outstanding dropped from 70.5m at the end of 2020 to 48.4m by the end of 2022.

Avis Budget Group is an outstanding example of a management team that are both good operators and capital allocators, stepping up their buybacks at the right time to return value to shareholders. They also purchased shares for their own accounts multiple times in 2021 and 2022, putting the stock on my radar through the Double Dipper screen.”

In the two years since the book was published, the company has continued to buy back shares but not at the rate it was doing during the pandemic. The stock is also up 33% since the publication date of May 21, 2024 but that is not even half the story.

Last month, the stock suddenly went parabolic, rising from nearly $146 at the end of March to an intraday peak of nearly $766 three weeks later. A short squeeze in a company with a very thin float triggered the massive move. The little P you see in late February on the chart below is a $40 million purchase by the merger arbitrage focused fund Pentwater Capital Management at an average price of $94.26.

Pentwater was already a 10% owner of Avis Budget Group before they added to their position and hence we were able to see that $40 million purchase from their Form 4 filing and didn’t have to wait for their 13F filing. At the end of Q1 2026, their 13F that was filed last Friday revealed a $922 million stake in the company through stock and call options that gave them exposure to another $113 million worth of stock. Interestingly, it also showed that they sold any put options they had on Avis Budget Group.

We have been following what a small group of merger arbitrage related funds have been doing each quarter and we published eight updates on their portfolio moves until August 2025. In my previous article titled Concentrated Merger Arbitrage Funds – Q2 2025 Update, I referenced Pentwater Capital’s portfolio (without naming them) and wrote the following:

“One of the eight merger arbitrage funds I track decided to start a new position in UnitedHealth Group and it was interesting to see them do this through long stock exposure as well as both call options and put options.

This was the same fund that had a massive negative bet on the overall market in Q1 2025 and seems to consistently get these calls, whether they are related to merger arbitrage or otherwise, right.”

This year, they once again got the Avis Budget trade right and exited a sizable chunk of their position during that April parabolic move, as I mentioned in this tweet:

Pentwater likely generated more than $1 billion in profits from this trade, even after giving back some profits to the company for violating the short-swing rule (buying and selling within a six month period). We track insiders who either willingly or unknowingly violate the short-swing rule in a custom screen we like to call the Flip Floppers.

I don’t know if this trade is a worthy successor to Gregory Zuckerman’s The Greatest Trade Ever but I am ready to crown Pentwater’s Matt Halbower the “new king of merger arbitrage”. Looking beyond the excitement of this trade, the 13F filing for Pentwater for Q1 2026 shows them focusing on their bread and butter by starting new positions in merger arbitrage situations like Danaher’s acquisition of Masimo (MASI) and Eli Lilly’s acquisition of Centessa Pharmaceuticals (CNTA), which we covered in detail as a spotlight idea in our May 2026 Special Situations newsletter.

Voluntary Disclosure: I hold a long position in Eli Lilly (LLY).

Disclaimer: Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.

The Special Situation Report is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.