More than two decades after leaving the Pacific Northwest, I still miss the natural beauty of Oregon and its friendly people. When public market investors think about the state next to Oregon, they mostly think about chips.

One of these two companies based in Idaho makes memory chips and the other one makes potato chips (borrowing from the British who call french fries, chips). And the one making memory chips is nearly 100 times the size of the other. Investors doubling down on the AI “picks and shovels” trade and cutting back on food in this new world of GLP-1 drugs partially explains the huge chasm between the two.

One of them saw its quarterly revenue increase 196%, while the other one barely kept pace with the GDP growth rate.

I have a long position in one of them and the second one has been on my watchlist for a long time.

Insiders, Activists and Stock Buybacks

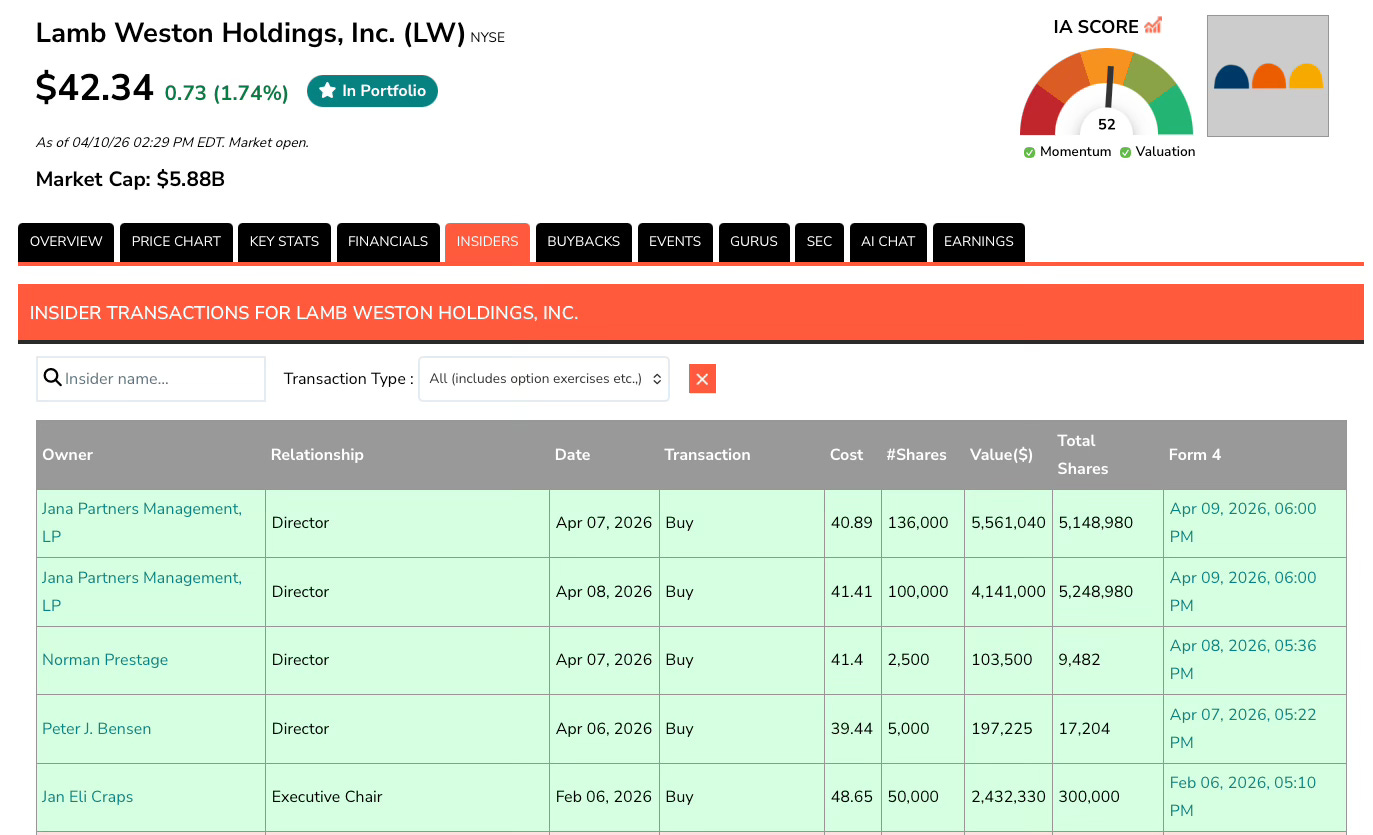

I was once again reminded of the Idaho-based potato products company Lamb Weston (LW) last night when we were looking at the latest crop of insider purchases. The activist investor Jana Partners added to their Lamb Weston stake to the tune of nearly $10 million. They were not the only insiders that were buying. Since the start of this year four different insiders have purchased shares including three this month.

Jana Partners has been involved with Lamb Weston since October 2024 and wanted the company to put itself up for sale. They also wanted Lamb Weston to improve operations and capital allocation. A few months later, Post Holdings (POST), the maker of mashed potatoes and cereals like Honey Bunches of Oats, started working with investment bankers to see if they could acquire Lamb Weston. By this point you had two special situations in play including activist involvement and the potential of an acquisition but unfortunately a sale did not materialize.

The company did however increase its stock buyback authorization by $250 million in December 2024, adding to its existing $500 million share repurchase authorization. The company did go ahead and execute on part of this buyback and has retired 2% of shares in the last five quarters.

Jana is not the only activist interested in the company and last month The Wall Street Journal reported that Starboard Value has built a sizable stake in Lamb Weston and is pushing the company to speed up improvements and cost-cutting to boost its underperforming stock.

Starboard is now one of the biggest shareholders in Lamb Weston. Starboard has been an investor in the company for a while and recently saw an opportunity to scoop up even more shares with the business looking undervalued.

Lamb Weston is a successful spinoff story with the company outperforming the S&P 500 by more than 100% since its spinoff from Conagra Brands (CAG) in November 2016.

The company has a long established leadership team with CEO Tom Werner working at Conagra for 17 years and shepherding Lamb Weston through the spinoff process.

Lamb Weston is one of the largest producers and processors of frozen potato products, including #1 in North America and #2 globally in the frozen potato category.

The company reported first quarter fiscal 2024 results that would turn even high growth SaaS companies green with envy. Net sales were up 48% and net income from operations was up 106%.

Net income margin of 14% is surprisingly strong for a food company.

The company recently announced a $500 million buyback program representing around 2.8% of its market cap at announcement.

I concluded the write up as follows:

“There is a lot to like about Lamb Weston including the fact that the company beat earnings estimates for eight quarters in a row and analysts have recently revised their estimates upwards. The main thing that gives me pause is the amount of debt they have on their balance sheet.

If we remain in a “higher for longer” interest rate environment, debt that matures will have to be refinanced at much higher rates. The company has also benefited from lapping results from a bad potato crop in 2022 and revenue growth may not continue at the pace we have seen in the recent past.

I am going to add the company to our watchlist to observe for a couple of quarters before making a decision about adding it to the model portfolio.”

Holding off on investing in Lamb Weston turned out to be the right decision as the stock lost more than half its value and declined from $89.52 to the current $42.34. Both revenue and earnings appear to have stabilized and the company is trading at a forward P/E below 14.

The Special Situation Report is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

While some investors might find this confluence of special situations (activists, insider buying and buybacks) interesting, it is the other chip company from Idaho that I have in my personal portfolio. Incidentally, despite a triple digit revenue growth rate and a net income margin that would turn most companies green with envy, the stock trades at a forward P/E of 7. Investors are concerned that this cyclical industry will once again see a big increase in supply and this company will come back down to earth.

Micron Technology (MU) has also seen insider buying this year and some of what we wrote about the company in an Insider Weekends article in January is as follows:

“Founded in Boise, Idaho in 1978 and the holder of over 60,000 patents, Micron Technology is a company that focuses on computer memory. They primarily sell two kinds of memory including the type that is used for your computer’s drive to store data (NAND) and the more rapid-access RAM memory that your computer uses (DRAM) as its temporary “working memory” while the CPU or GPU is computing data.

Think of the distinction as your brain using working memory to keep track of which cards have been previously played in a game of bridge or blackjack (DRAM or working memory that is not retained after the power is turned off) and the words you need to remember as you are learning a new language (NAND or stored memory that is still accessible after your phone or computer are switched off).

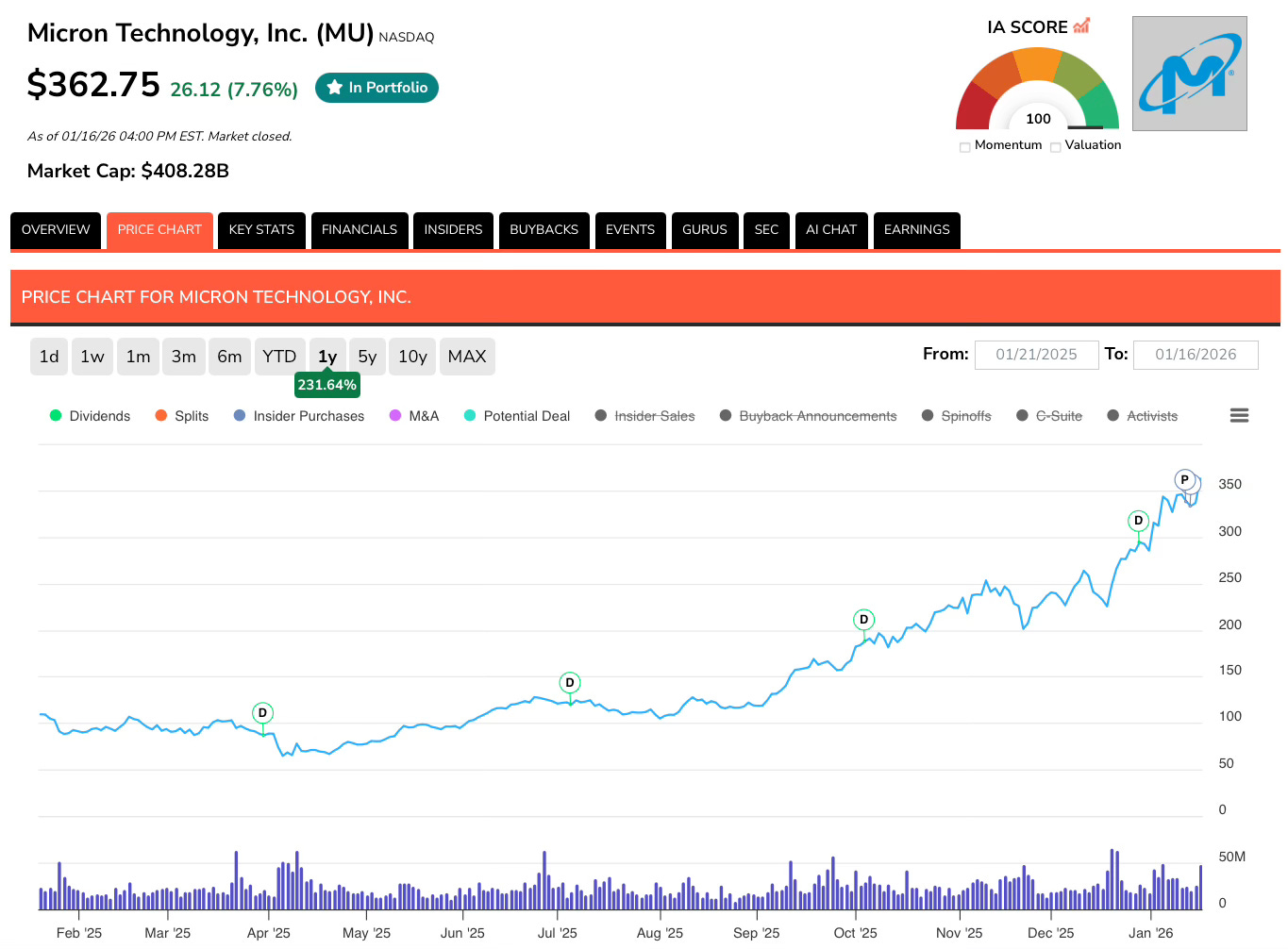

The stock, which at one point during the tariff-related fears of last April, had dipped below $65 has recently gone parabolic and trades at $362.75. Incidentally the company also scores a perfect 100 in our IA Score quant model.”

Why the Sudden Acceleration?

At an investor pitch lunch in July 2024, a friend who works at Google pitched Micron because he felt that the “high bandwidth memory” or HBM, which was specifically developed for applications like AI/machine learning and high-performance computing in conjunction with GPUs, would benefit companies like Micron that produce them.

He mentioned that NVIDIA’s Blackwell B200, which was announced in 2024 would have 192 GB of onboard memory. Another friend, also picked Micron during an investor lunch in early 2025 for the same reason. NVIDIA Blackwell Ultra B300, which was announced in March 2025 had capacity for 288 GB of onboard memory.

While traditional NAND memory was going through pricing pressures due to the cyclical nature of flash memory, HBM had pricing power due to the big increase in demand related to GPUs and Google’s custom developed processors Tensor Processing Units (TPUs).

All of that changed towards the end of 2025 as demand for GPUs and memory started going through the roof with projects like OpenAI’s Stargate locking up supply. Micron mentioned that it is sold out of memory for 2026 and has had to move production from traditional memory for computers and devices, to HBM. This CNBC article sums up the situation well.

This shift created a tailwind for NAND memory as well and was a contributing factor in SanDisk’s (SNDK) 751% rise since its spinoff from Western Digital (WDC) last February. We covered that spinoff in the October 2024 newsletter.

Insider Purchase

The insider purchase last week that prompted us to pick Micron for this week’s Insider Weekends article was the largest purchase Micron has ever seen over the last fifteen years. Director Teyin Liu had 2,710 shares before he decided to pick up 23,200 shares at an average price of $337.14 for $7.82 million.

This is his first insider purchase of Micron since he joined the board in March 2025 and is also the first insider purchase of any kind at Micron in over eight years. The only other insider who purchased shares during the last fifteen years was Micron’s former CFO Ernest Maddock who picked up shares between 2015 and 2017 in a series of small transactions and then retired from the company in 2018.

On a related note, Ernest Maddock scores a perfect 100 in our system that ranks insiders and has generated an IRR of nearly 165% on his infrequent insider purchases of Micron (MU), Ouster (OUST), Teradyne (TER) and Ultra Clean Holdings (UCTT).

Who is Teyin Liu?

Last week as we were working through the insider transactions filed on Thursday to get the Event-Driven Monitor for January 16th ready, we were struck by both the size of this Micron purchase and the fact that an insider was willing to buy after such a big run-up in the stock. I clicked on the AI Chat button on Teyin Liu’s page to see when he joined Micron’s board (new directors often buy stock and we view that as a weak signal) and what his background was.

Mr. Liu spent 30 years at TSMC where he was the Co-COO from 2012 to 2013 and then Co-CEO from 2013 to 2018 before becoming the Executive Chairman from 2018 to 2024. He received his Ph.D. in Electrical Engineering and Computer Science from University of California, Berkeley and started his career at Intel.

Given his vast experience, his insider purchase signals that he sees additional value in Micron in the upcoming quarters.

I believe that the trend we are seeing in memory demand is likely to continue but am not so sure the industry will become a secular growth story like we saw with the broader semiconductor industry, which itself transitioned from cyclical to secular growth. If you think the AI hype is overblown and would prefer to invest in real businesses, then it would be worth exploring why both Starboard Value and Jana Partners are excited about Lamb Weston and if there is a potential acquisition on the horizon.

The Special Situation Report is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Disclaimer: I hold a long position in Micron. Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.

French fries and high bandwidth memory chips- an interesting meal. A nice write up my friend. See you here in Vegas in a few months 😏👊